Questions for the Variable (Stabilized) Benefit Plan fans in the audience -

1 - If, in a post-2006 PPA world, we are "now left with a pension that is massively expensive and the fundamentals were not built around the new regulations" and "It’s massively expensive to raise the benefit" of our current A-plan, could you please explain (or have our actuarial firm explain)

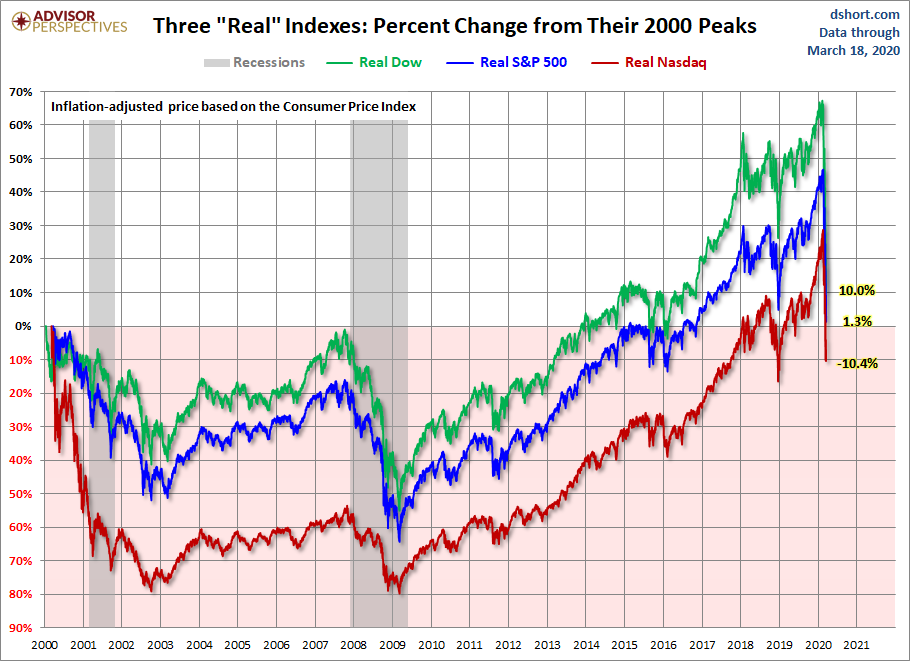

how we can still have a 2006 PPA-compliant DB fund that qualifies as a PBGC protected fund based on its underlying investments and NOT be subjected to the same massively expensive funding requirements to improve it? Is it through the power of stock market investments? Would you be surprised to find out that from the time of the 1999 contract that is referenced in this discussion through March 23, 2019 the S&P/Dow/NASDAQ are essentially at REAL NEGATIVE RATES OF RETURN?? (This chart is from 2000 - March 18th, so the Dow is down another 2000 pts/10% from that although it's back up a bit until tomorrow) How is all of this future wealth possible with the V/SB plan without a much higher price tag without going to the casino? Is stock market exposure/risk really the missing ingredient that company is not properly utilizing to increase our retirement checks?

1a - The PBGC issue used to be a joke, like "if FedEx retirees are needing the PBGC payout then the country is going down the tube and civilization is coming to an end." Current events now dictate that PBGC protection needs to be understood beyond a doubt with a V/SB plan investment structure that relies more heavily on risky stocks. Will the V/SB plan even qualify as a DB plan because it does not have a "defined benefit" per se? If you read the PBGC website, this plan does not fit in the description of any DB covered plans. If our V/SB plan loses 30+% of its assets like is going on in the stock market as we speak, does the company have to make up the difference in cash to comply with funding requirements or pay much higher PBGC premiums? Even if we only get 30% PBGC retirement check for the remainder of our lives due to bankruptcy/plan termination, it is better than 0 amiright?

2 - Is it really that easy to "change the formula" we use to calculate our liabilities to circumvent the PPA funding requirements so the company doesn't have to contribute as much yet our lifetime annuity increases? Inconceivable! Seems like a pathway to fines or lawsuits or disqualification from "pension" status and disappointed retiring pilots. Seems like we might even disqualify ourselves from the 06 PPA requirements of pensions and possibly expose our legally protected fund to unknown risk. If this gets "Munsoned" does it expose anyone in particular to lawsuits for fiduciary negligence?

3 - Do you personally share the actuarial firm's threshold of acceptable risk, even after the seven sigma events of the last 2 months? If so, you probably wouldn't be as concerned as I am that their website tells employers that V/SB funds are great because employers can "Expect stable annual contributions because

you share investment risks with covered employees." ie, you and me taking it in the wallet. Don't you like having an A fund that is as protected from stock market risk and a B fund that you can subject to all the risk you want? That chart above shows near real negative rates of return on those indexes over the last 21 years, and no fund manager can consistently beat those indexes and pilots are a million times worse than they are when it comes to investing! In many ways, a rock solid A plan protects us from ourselves!

4 - Don't you think that sometimes doing nothing is better than doing something in a panic? Shouldn't we let this carnage and cleansing of the financial system and airline industry that many of our friends are having to endure run its course before we put all our chips in on an untested retirement system? Please understand the MLB has nothing like this whatsoever and we would be the first "millionaire" test group of this thing. Maybe we should get serious about improving our current A plan and B plan and not go to the casino because the company said "no." If we are furloughed for multiple years how does that effect getting paid for every hour flown calculations in the V/BS plan? If the company has skated by since the 06 contract without having to improve our A plan thereby benefitting from inflation while we did took a hit, maybe it's time that they are asked to distribute some of that ROI towards maintaining our standard of living in our short retirement years. A-plans are expensive, no doubt about it. But isn't that a cost of moving high priority cargo to every corner of the world? Let the company fund our A plan improvements from our profits we can play day-trader with our B plans.

Those are questions for the supporters of the V/BS plan, and I hope you can explain it because I have not had those questions satisfactorily asked or answered by anyone.

Final question...

5 - Where did all of the V/BS literature from the actuarial firm go on the FDX Alpa website go? It used to be the most prominent topic but now it is completely scrubbed (or am I looking in the wrong place?).

Knibb High Football Rules! Dr K.