Any "Latest & Greatest" about Delta?

03-18-2011 | 05:49 AM

03-18-2011 | 05:49 AM

Happy to be here

Joined: Jun 2006

Posts: 18,563

Likes: 0

From: A-320A

A few prognosticators, including a hedge fund manager, are predicting doom and gloom coming in Delta's March 22 Raymond James presentation. Significance is seen in the timing of the presentation prior to the opening of the market.

I've been increasingly aware of a call for management to "do something" to stop the erosion of Delta's share price which has been declining even with fuel prices adjusting down. Economists are saying fuel, if not for Japan, would be about $130Bbl on the coasts. Maybe that is what the market sees, or perhaps they are just concerned about an overall slow down in economic activity, which tends to have a larger effect on the airlines than other entities.

Given that United/CAL, US Air and American have all pulled some capacity (leaving room for the LCC to grow btw) my guess is that we'll hear an announcement of reduced capacity as our mainline jets are retired in favor of outsourced flying in smaller capacities. The mega big bid which was going to allegedly happen about now will likely hold us about status quo. It would not surprise me to see CVG close, but I am not expecting it.

Anyone else got a guess?

I've been increasingly aware of a call for management to "do something" to stop the erosion of Delta's share price which has been declining even with fuel prices adjusting down. Economists are saying fuel, if not for Japan, would be about $130Bbl on the coasts. Maybe that is what the market sees, or perhaps they are just concerned about an overall slow down in economic activity, which tends to have a larger effect on the airlines than other entities.

Given that United/CAL, US Air and American have all pulled some capacity (leaving room for the LCC to grow btw) my guess is that we'll hear an announcement of reduced capacity as our mainline jets are retired in favor of outsourced flying in smaller capacities. The mega big bid which was going to allegedly happen about now will likely hold us about status quo. It would not surprise me to see CVG close, but I am not expecting it.

Anyone else got a guess?

I would imagine the revised guidance will be lower (there's a surprise), and I've had the same thought about the timing. But then again, United is presenting at 11:05 AM, and UsAirways at 10:25 AM. Does that mean they expect good results? ... so I think the timing relates more to scheduling and coincidence than anything else.

My guess is that we will say that we're leading the industry in capacity retsraint, have already announced accelerated retirements of less fuel-efficient fleets, will consider further cuts as needed, are reducing CAPEX to a more prudent level, but will continue to invest in the product. Growth guidance of flat may not do the trick, so we'll forecast down 1-3% (pulling all this out of thin air). Since we go up first on most conferences, and on quarterly results, since we're 84% owned by institutional investors, and since we got spanked two quarters ago by not sounding negative enough on capacity, my guess is it will quite the sobering talk. "Growth" will be a taboo word, and every sentence will feature the term "capacity restraint" at least once.

I doubt CVG goes, but who knows? The AE will be delayed, or be roughly neutral, as the company stays in a defensive posture.

At any rate, if any gloom and doom comes forth, it won't be a surprise to anyone that invests in airline stocks. I'm guessing the bad news in the stock in mostly baked in, and maybe it goes down further Monday, and up after the conference. I am, however, also guessing the sobering news will ding the carriers perceived as being weaker. I had added AMR stock, but I took the loss on most of it and sold for now.

My guess is that we will say that we're leading the industry in capacity retsraint, have already announced accelerated retirements of less fuel-efficient fleets, will consider further cuts as needed, are reducing CAPEX to a more prudent level, but will continue to invest in the product. Growth guidance of flat may not do the trick, so we'll forecast down 1-3% (pulling all this out of thin air). Since we go up first on most conferences, and on quarterly results, since we're 84% owned by institutional investors, and since we got spanked two quarters ago by not sounding negative enough on capacity, my guess is it will quite the sobering talk. "Growth" will be a taboo word, and every sentence will feature the term "capacity restraint" at least once.

I doubt CVG goes, but who knows? The AE will be delayed, or be roughly neutral, as the company stays in a defensive posture.

At any rate, if any gloom and doom comes forth, it won't be a surprise to anyone that invests in airline stocks. I'm guessing the bad news in the stock in mostly baked in, and maybe it goes down further Monday, and up after the conference. I am, however, also guessing the sobering news will ding the carriers perceived as being weaker. I had added AMR stock, but I took the loss on most of it and sold for now.

All of this stated, loads look good, and ppl are traveling. Full again going to Europe tonight.

03-18-2011 | 05:59 AM

Gets Weekends Off

Joined: Jun 2009

Posts: 5,113

Likes: 0

They will of course have to give the street some red meat, some kind of headline number to make them "happy", which is why I'm guessing -1 to -3% capacity, or some news about a fuel surcharge program, or some kind of action that analysts can use to chew on and make powerful statements about.

03-18-2011 | 06:05 AM

seeing the country...

Joined: Oct 2006

Posts: 4,015

Likes: 41

From: 73N A

My guess is that we will say that we're leading the industry in capacity retsraint, have already announced accelerated retirements of less fuel-efficient fleets, will consider further cuts as needed, are reducing CAPEX to a more prudent level, but will continue to invest in the product. Growth guidance of flat may not do the trick, so we'll forecast down 1-3% (pulling all this out of thin air). Since we go up first on most conferences, and on quarterly results, since we're 84% owned by institutional investors, and since we got spanked two quarters ago by not sounding negative enough on capacity, my guess is it will quite the sobering talk. "Growth" will be a taboo word, and every sentence will feature the term "capacity restraint" at least once.

")

It's all about making them *think* we're reducing capacity.

03-18-2011 | 06:10 AM

Gets Weekends Off

Joined: Jun 2009

Posts: 5,113

Likes: 0

03-18-2011 | 06:32 AM

03-18-2011 | 06:32 AM

Can't abide NAI

Joined: Jun 2007

Posts: 12,078

Likes: 15

From: Douglas Aerospace post production Flight Test & Work Around Engineering bulletin dissembler

Which is a position I do not understand.

Reduced capacity results in mush higher unit costs for the remaining capacity. While over expansion surely means death, so does continual retreat.

As we seem to cede the point to point O&D domestic, we become nothing more than a thin network to feed our international operations.

But, that simply exposes us to a greater risk:

IMHO, shrinking is the most risky course we could take. Eventually we will run out of places to consolidate.

Reduced capacity results in mush higher unit costs for the remaining capacity. While over expansion surely means death, so does continual retreat.

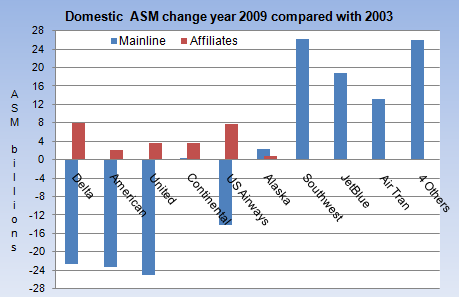

According to data released last month from AirFinancials.com, domestic carrying capacity for the nation's legacy carriers declined by 85 billion available seat miles between 2003 and 2009, or by 21% on average. Over the same period, domestic capacity among low-cost carriers Southwest Airlines /quotes/comstock/13*!luv/quotes/nls/luv (LUV 12.22, +0.37, +3.12%) , JetBlue Airways /quotes/comstock/15*!jblu/quotes/nls/jblu (JBLU 5.78, +0.15, +2.66%) , AirTran and four other small carriers rose by more than 84 billion available seat miles.

That's not necessarily a bad thing. Most of those domestic routes the legacy carriers gave up had slim profit margins that the budget carriers were able to widen through their lower-cost model. The real money for the legacy carriers is in the international routes, particularly as it relates to premium-paying business travel.

Delta Air Lines, Trippler notes, appears to be concentrating exclusively on international, while airlines such as Southwest and AirTran have become feeders into the major airport hubs.

"So over the next five years the legacies will become more like trunk carriers with smaller airlines feeding people into the hubs," he said.

That's not necessarily a bad thing. Most of those domestic routes the legacy carriers gave up had slim profit margins that the budget carriers were able to widen through their lower-cost model. The real money for the legacy carriers is in the international routes, particularly as it relates to premium-paying business travel.

Delta Air Lines, Trippler notes, appears to be concentrating exclusively on international, while airlines such as Southwest and AirTran have become feeders into the major airport hubs.

"So over the next five years the legacies will become more like trunk carriers with smaller airlines feeding people into the hubs," he said.

But, that simply exposes us to a greater risk:

Originally Posted by ATW

At the heart of the matter is the rapid growth of the carriers of the Persian Gulf region with their deep-pocket state owners and global ambitions (ATW, 7/10, p. 5). To Assn. of European Airlines Secretary General Ulrich Schulte-Strathaus, Emirates, Etihad and Qatar represent a new type of competitive threat that is incompatible with the existing world aviation order. That’s the message he brought to the International Aviation Club in Washington recently.

The carriers, “two of which have never made a profit” (a reference to Etihad and Qatar), are “operated as an instrument of national strategy and integrated vertically across commerce, tourism and foreign policy,” he declared.

To their owners, Schulte-Strathaus said, they are “just a part—a tool—of this vertically integrated economic chain,” and they are “being driven by a policy which is not compatible with that of the US and Europe,” or “Australia, China, Japan, Canada, Mexico, Brazil, Chile, Korea and so on.” Furthermore, these carriers will take 425 widebodies over the next five years, more than are currently operated by the US major airlines.

The carriers, “two of which have never made a profit” (a reference to Etihad and Qatar), are “operated as an instrument of national strategy and integrated vertically across commerce, tourism and foreign policy,” he declared.

To their owners, Schulte-Strathaus said, they are “just a part—a tool—of this vertically integrated economic chain,” and they are “being driven by a policy which is not compatible with that of the US and Europe,” or “Australia, China, Japan, Canada, Mexico, Brazil, Chile, Korea and so on.” Furthermore, these carriers will take 425 widebodies over the next five years, more than are currently operated by the US major airlines.

03-18-2011 | 06:38 AM

Can't abide NAI

Joined: Jun 2007

Posts: 12,078

Likes: 15

From: Douglas Aerospace post production Flight Test & Work Around Engineering bulletin dissembler

Along the lines of the article above is Herbst's Chart on Seeking Alpha:

This would certainly make for interesting talk over the water cooler in the CAL / United SLI debate.

This would certainly make for interesting talk over the water cooler in the CAL / United SLI debate.

03-18-2011 | 06:40 AM

Happy to be here

Joined: Jun 2006

Posts: 18,563

Likes: 0

From: A-320A

Which is a position I do not understand.

Reduced capacity results in mush higher unit costs for the remaining capacity. While over expansion surely means death, so does continual retreat.

As we seem to cede the point to point O&D domestic, we become nothing more than a thin network to feed our international operations.

But, that simply exposes us to a greater risk:

IMHO, shrinking is the most risky course we could take. Eventually we will run out of places to consolidate.

Reduced capacity results in mush higher unit costs for the remaining capacity. While over expansion surely means death, so does continual retreat.

As we seem to cede the point to point O&D domestic, we become nothing more than a thin network to feed our international operations.

But, that simply exposes us to a greater risk:

IMHO, shrinking is the most risky course we could take. Eventually we will run out of places to consolidate.

03-18-2011 | 06:41 AM

seeing the country...

Joined: Oct 2006

Posts: 4,015

Likes: 41

From: 73N A

I know, but they must be thinking that tighter capacity means higher RASM. Sure - in a bubble, but Southwest, Jetblue, Virgin America, Spirit and Alligent waiting to pounce on the routes we drop. It's frustrating.

03-18-2011 | 07:00 AM

Happy to be here

Joined: Jun 2006

Posts: 18,563

Likes: 0

From: A-320A

SWA has been able to constantly spread their higher costs over more seats, and that is why that up to a few years ago, they were able to look really good on paper. They still are very well run, but absent taking over the international market, they are capped out with regard to their old model. IMO, they realize this, and that is why they bought ATN.

03-18-2011 | 07:10 AM

Gets Weekends Off

Joined: Aug 2010

Posts: 2,530

Likes: 0

But, that simply exposes us to a greater risk:

IMHO, shrinking is the most risky course we could take. Eventually we will run out of places to consolidate.

Originally Posted by ATW

At the heart of the matter is the rapid growth of the carriers of the Persian Gulf region with their deep-pocket state owners and global ambitions (ATW, 7/10, p. 5). To Assn. of European Airlines Secretary General Ulrich Schulte-Strathaus, Emirates, Etihad and Qatar represent a new type of competitive threat that is incompatible with the existing world aviation order. That�s the message he brought to the International Aviation Club in Washington recently.

The carriers, �two of which have never made a profit� (a reference to Etihad and Qatar), are �operated as an instrument of national strategy and integrated vertically across commerce, tourism and foreign policy,� he declared.

To their owners, Schulte-Strathaus said, they are �just a part�a tool�of this vertically integrated economic chain,� and they are �being driven by a policy which is not compatible with that of the US and Europe,� or �Australia, China, Japan, Canada, Mexico, Brazil, Chile, Korea and so on.� Furthermore, these carriers will take 425 widebodies over the next five years, more than are currently operated by the US major airlines.

IMHO, shrinking is the most risky course we could take. Eventually we will run out of places to consolidate.

Originally Posted by ATW

At the heart of the matter is the rapid growth of the carriers of the Persian Gulf region with their deep-pocket state owners and global ambitions (ATW, 7/10, p. 5). To Assn. of European Airlines Secretary General Ulrich Schulte-Strathaus, Emirates, Etihad and Qatar represent a new type of competitive threat that is incompatible with the existing world aviation order. That�s the message he brought to the International Aviation Club in Washington recently.

The carriers, �two of which have never made a profit� (a reference to Etihad and Qatar), are �operated as an instrument of national strategy and integrated vertically across commerce, tourism and foreign policy,� he declared.

To their owners, Schulte-Strathaus said, they are �just a part�a tool�of this vertically integrated economic chain,� and they are �being driven by a policy which is not compatible with that of the US and Europe,� or �Australia, China, Japan, Canada, Mexico, Brazil, Chile, Korea and so on.� Furthermore, these carriers will take 425 widebodies over the next five years, more than are currently operated by the US major airlines.

FlightAware > Live Emirates Flight Status

5 flights (1100 EST) all to/from DXB - US. It's only going to grow.

Thread

Thread Starter

Forum

Replies

Last Post