View Poll Results: Will AA declare bankruptcy?

Yes

219

70.65%

No

91

29.35%

Voters: 310. You may not vote on this poll

Bankruptcy

03-17-2021 | 10:14 PM

03-17-2021 | 10:14 PM

#411

Gets Everyday Off

Joined: Aug 2016

Posts: 6,995

Likes: 1

From: Fully Retired

From today’s WSJ:

https://www.wsj.com/articles/america...hs-11615973407

“No major debt” is in the eye of the beholder. I believe there is $500 million due this year and $750 million next year, both of which can probably be refinanced by another bond sale, albeit probably at a higher coupon. But most of the big bond issueswill mature in 2023 and later.

https://www.wsj.com/articles/america...hs-11615973407

“No major debt” is in the eye of the beholder. I believe there is $500 million due this year and $750 million next year, both of which can probably be refinanced by another bond sale, albeit probably at a higher coupon. But most of the big bond issueswill mature in 2023 and later.

After that, management is counting on strong profits to yield enough cash flow to meet big time debt repayment. It is a roll of the dice, but I think the odds of success are a lot better than Vegas gives you.

03-18-2021 | 02:49 AM

#412

Gets Weekends Off

Joined: Jul 2017

Posts: 1,729

Likes: 0

Well, the difficulty with excessive debt is that as the credit rating goes down, the debt service tends to go up. Nothing wrong with taking on debt for an asset that can be used to make money in the business. It’s like buying a house to rent, as long as the rent payment a little more than covers the mortgage, it’s OK. But the problem with having debt in this environment is that - through no fault of the borrower - the ‘rent’ just isn’t there.

Worse yet, you got good terms from the lender because you collateralized those bonds with shiny new airplanes at a time when the waiting list for new aircraft was long and the market for used aircraft was similarly high. But it will be five years (or ten years) later pretty soon and - again through no fault of the borrower - COVID has kept those aircraft from being gainfully employed, increased the debt, and driven down the liquidity of the borrower. So now the money isn’t there to pay off the bonds when they mature, so you HAVE to refinance them with another bond issue to pay off the original one. Except now the aircraft aren’t new and shiny, they are five (or ten) year old USED aircraft, and that makes their market (and collateral) value less and even at that, the used aircraft market is flooded and so you wind up needing to sell the new bonds at a higher coupon rate.

which increases your debt service cost without decreasing your debt.

Worse yet, you got good terms from the lender because you collateralized those bonds with shiny new airplanes at a time when the waiting list for new aircraft was long and the market for used aircraft was similarly high. But it will be five years (or ten years) later pretty soon and - again through no fault of the borrower - COVID has kept those aircraft from being gainfully employed, increased the debt, and driven down the liquidity of the borrower. So now the money isn’t there to pay off the bonds when they mature, so you HAVE to refinance them with another bond issue to pay off the original one. Except now the aircraft aren’t new and shiny, they are five (or ten) year old USED aircraft, and that makes their market (and collateral) value less and even at that, the used aircraft market is flooded and so you wind up needing to sell the new bonds at a higher coupon rate.

which increases your debt service cost without decreasing your debt.

03-18-2021 | 04:34 AM

#413

Eating A Gruben

Joined: Feb 2020

Posts: 1,065

Likes: 0

His point is that debt is acceptable (and even good) if what you went into debt to acquire pays the costs of ownership. It’s not an exact comparison, no one buys planes to make money off them. The depreciation is built into the economics of purchasing the airplane.

03-18-2021 | 05:27 AM

#414

Line Holder

Joined: Jan 2014

Posts: 1,550

Likes: 146

While that’s true, what’s that have to do with what he’s saying?

His point is that debt is acceptable (and even good) if what you went into debt to acquire pays the costs of ownership. It’s not an exact comparison, no one buys planes to make money off them. The depreciation is built into the economics of purchasing the airplane.

His point is that debt is acceptable (and even good) if what you went into debt to acquire pays the costs of ownership. It’s not an exact comparison, no one buys planes to make money off them. The depreciation is built into the economics of purchasing the airplane.

03-18-2021 | 07:23 AM

#415

Perennial Reserve

Joined: Jan 2018

Posts: 14,237

Likes: 254

Compared to $50 billion in total debt, $500 million and $750 million probably qualify as “no major debt” needing to be repaid before 2023. That is only 2 - 3% of the overall debt.

After that, management is counting on strong profits to yield enough cash flow to meet big time debt repayment. It is a roll of the dice, but I think the odds of success are a lot better than Vegas gives you.

After that, management is counting on strong profits to yield enough cash flow to meet big time debt repayment. It is a roll of the dice, but I think the odds of success are a lot better than Vegas gives you.

03-18-2021 | 01:15 PM

#416

You scratched my anchor

Joined: Feb 2011

Posts: 5,126

Likes: 84

03-18-2021 | 01:58 PM

#417

Perennial Reserve

Joined: Jan 2018

Posts: 14,237

Likes: 254

Parker on how AA is positioned with its debt:

https://www.google.com/amp/s/seeking...hmMG5ENJ37DOnw

https://www.google.com/amp/s/seeking...hmMG5ENJ37DOnw

03-20-2021 | 01:29 AM

03-20-2021 | 01:29 AM

#418

Gets Weekends Off

Joined: Nov 2013

Posts: 1,775

Likes: 0

Here's another expert on how eff'd we're all are:

(please click on the link, I can only post with three pictures, the article has about 10 graphs)

link

There was, perhaps, no industry more impacted by COVID than airlines. Of course, many types of businesses - particularly travel-related ones - were devastated by the faucet simply being turned off in a series of unprecedented moves by governments globally. Airlines, however, operate in a cut-throat, razor-thin margin business during good times, so 2020 was particularly nasty for them.

However, the light has appeared at the end of the tunnel, beginning with November's announcement that a successful vaccine was on the way. Since then, shares of coach class legend American Airlines Group (AAL) have more than doubled.

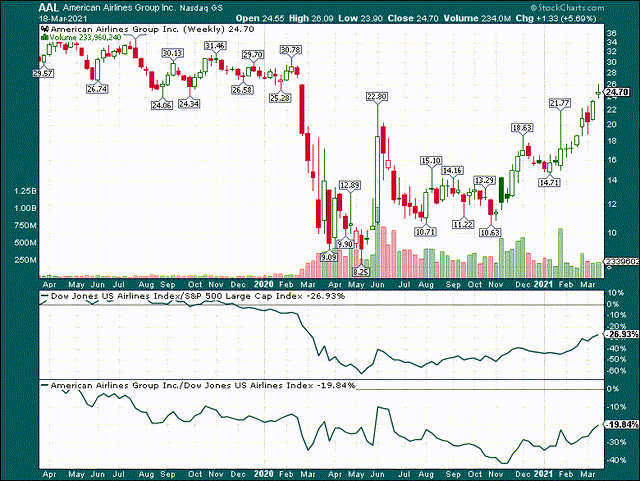

Indeed, if we draw a line in the sand in early November of last year, we can see that the airlines as a group have outperformed the S&P 500 by about 25%, and on top of that, American has outperformed the airlines by about 20%. In other words, American is flying (bad joke: I'll see myself out).

However, if we zoom out to the two-year chart above, we can see that there should be significant selling pressure on American in the near term simply because all of the people that bought in 2019 will now be at the point where they have more or less gotten their money back. Normally when a stock sees a massive decline and then recovery, price action churns when the stock returns to pre-crash levels. I expect that the enormous amount of supply in the mid-20s and up will be a problem for bulls. That doesn't mean American is doomed, but it does mean that the likelihood of this rally continuing at its current pace is extremely unlikely.

Apart from that, I just think American is very expensive, and is pricing in a recovery that may or may not come. In addition to that, the recovery is already years away under a rosy scenario; what if things don't work out as planned? For these reasons, I think American should be sold. I won't go as far as saying I'm bearish because airline stocks with high short interest are battlegrounds today, and anything can happen. But for long-term shareholders, your money deserves better; permit me to elaborate.

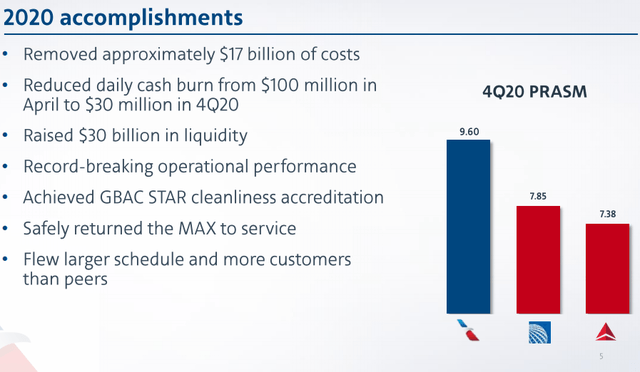

Part of that suffering was job losses that accrued from massive losses in places like airlines, which American certainly partook in. We're all aware of how poorly American performed last year so I don't need to rehash it, but on the bright side, some good came of it.

Source: Investor presentation

American removed $17 billion (!) in costs in 2020, and reduced its daily cash burn by 70% from the worst of the pandemic to the end of the year. This, of course, was a massive concern in the early stages of the crisis because airlines have enormous infrastructure that is costly to operate, which includes payroll. However, government measures and capital raises have kept the airlines afloat, and in my view, there are no liquidity/solvency concerns for American at this point. That's good, but it doesn't make the stock a buy; it just means there is no impending disaster.

Speaking of disaster, revenue could certainly be described as such for last year.

American had been producing nice, steady growth in the top line in the years prior to 2020, but of course, that all came tumbling down beginning in mid-March. Revenue was but a tiny fraction of what it was supposed to be, and even this year, which should see some return to normal, expected revenue is still just over half what it was in 2019. 2022 is slated to show another sizable rebound, but still nothing close to what American produced pre-pandemic.

Revisions aren't exactly bullish, either. In fact, revenue for this year continues to fall, even after the vaccine was announced. The timetable for a return to a normal flight schedule continues to be pushed back, and the revision trends above show you what that looks like in practice.

Buyers of the stock today - at very close to pre-pandemic levels - are essentially betting that these numbers suddenly reverse higher and take earnings with them; I'm simply unwilling to do that based upon the evidence I see.

Now, bookings are undoubtedly improving, and that's good news for a variety of reasons, whether you're a shareholder or not. We all want "normal" to come back and this data is a step in the right direction. But let's keep in mind that traffic is still less than half what it was in 2019, and that bookings for American continue to trend well below pre-pandemic levels. These numbers will continue to improve, undoubtedly, but we are still simply trying to get off the bottom. Bidding the stock up to new 52-week highs because a little bit of recovery is taking place seems extremely premature to me.

Here's an interesting look at where American sees the recovery, and again, I think it just points to how premature the rally in the shares is at this point.

I don't need to read this to you but basically, American is a very long way from a return to normal. And if we consider the domestic business stage of the recovery, it stands to reason that at least some of that traffic may never return. The world has proven it can operate without face-to-face interaction, so will companies continue to spend billions of dollars collectively on air travel that can be largely replaced with a video call? I don't think so, but American is pricing that in.

To be fair, American is almost certain to see margin improvements whenever "normal" comes back.

Not only does it have the cost savings identified above, but it has accelerated its fleet renewal/retirement program, so its fleet should be far more efficient in the coming years than it was going into the crisis. Those are good things, and should not be ignored. However, as we'll see below, based upon where the revenue situation is related to the valuation of the stock, these margin improvements simply aren't enough.

American has always carried a huge amount of debt, but this problem has been exacerbated by the crisis. The company is paying more than a billion dollars annually just to service debt, and longer term, there is simply no capacity for this company to ever pay off a meaningful amount of it. Even if American simply wants to get back to its pre-crisis level of net debt, it needs to come up with ~$8 billion, or about 2.5 years of pre-crisis annual operating income. It will also make it more difficult for American to borrow in the future because it is already hugely leveraged at this point.

In addition, American has issued a sizable number of shares since the crisis began, as we can see below.

The share count has soared from 423 million a year ago to 640 million by December; I don't know what the share count will be for the end of March, but it won't be anything close to 423 million. That means massive dilution to shareholders, making an earnings recovery that much more difficult. Indeed, with 50% more shares outstanding, American has to now earn 50% more on a dollar basis to simply equal what the figure would have been under the old share count. Perhaps more than any other headwind, this one is significant.

For context, because of recent price movement and the higher share count, American's market cap is now higher than it was pre-crisis; that logically makes absolutely no sense given all of the problems American has today.

Source: Seeking Alpha

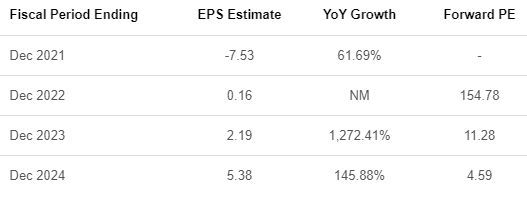

Next year, consensus is for breakeven, roughly, followed by a small profit in 2023. By 2024, a normalized profit is expected, but that is three years from now. Bulls will surely look at the P/E ratio of 4.6 on 2024 earnings and lick their figurative chops, but as we can see below, that's not even that cheap.

This is a six-year look at American's forward P/E ratio prior to COVID-19, and should be a strong guide for how American will be valued coming out of the crisis. We can see that the lower bound was just over 4X, with the upper bound at 11X. Average was in the middle at 7X earnings, but let's keep in mind that American is trading for 4.6X projected earnings for three years from now. On that basis, the stock looks incredibly expensive to me, particularly considering the following: an uncertain future of business travel, nearly $30 billion in net debt, and an as yet undetermined return to normal time frame.

Putting all of this together, and a nearly full valuation on 2024 earnings estimates, the signal is clear; American is grossly overvalued, and the stock is a sell.

This article was written by

Josh Arnold

(please click on the link, I can only post with three pictures, the article has about 10 graphs)

link

American Airlines Has Problems On Top Of Problems

Mar. 19, 2021 11:39 AM ETAmerican Airlines Group Inc. (AAL)17 Comments2 LikesSummary

- AAL continues to rally hard.

- But, I see lots of resistance just above the current price.

- In addition, there are several fundamental reasons the current rally should not be supported.

There was, perhaps, no industry more impacted by COVID than airlines. Of course, many types of businesses - particularly travel-related ones - were devastated by the faucet simply being turned off in a series of unprecedented moves by governments globally. Airlines, however, operate in a cut-throat, razor-thin margin business during good times, so 2020 was particularly nasty for them.

However, the light has appeared at the end of the tunnel, beginning with November's announcement that a successful vaccine was on the way. Since then, shares of coach class legend American Airlines Group (AAL) have more than doubled.

Indeed, if we draw a line in the sand in early November of last year, we can see that the airlines as a group have outperformed the S&P 500 by about 25%, and on top of that, American has outperformed the airlines by about 20%. In other words, American is flying (bad joke: I'll see myself out).

However, if we zoom out to the two-year chart above, we can see that there should be significant selling pressure on American in the near term simply because all of the people that bought in 2019 will now be at the point where they have more or less gotten their money back. Normally when a stock sees a massive decline and then recovery, price action churns when the stock returns to pre-crash levels. I expect that the enormous amount of supply in the mid-20s and up will be a problem for bulls. That doesn't mean American is doomed, but it does mean that the likelihood of this rally continuing at its current pace is extremely unlikely.

Apart from that, I just think American is very expensive, and is pricing in a recovery that may or may not come. In addition to that, the recovery is already years away under a rosy scenario; what if things don't work out as planned? For these reasons, I think American should be sold. I won't go as far as saying I'm bearish because airline stocks with high short interest are battlegrounds today, and anything can happen. But for long-term shareholders, your money deserves better; permit me to elaborate.

American Is Doing What It Can

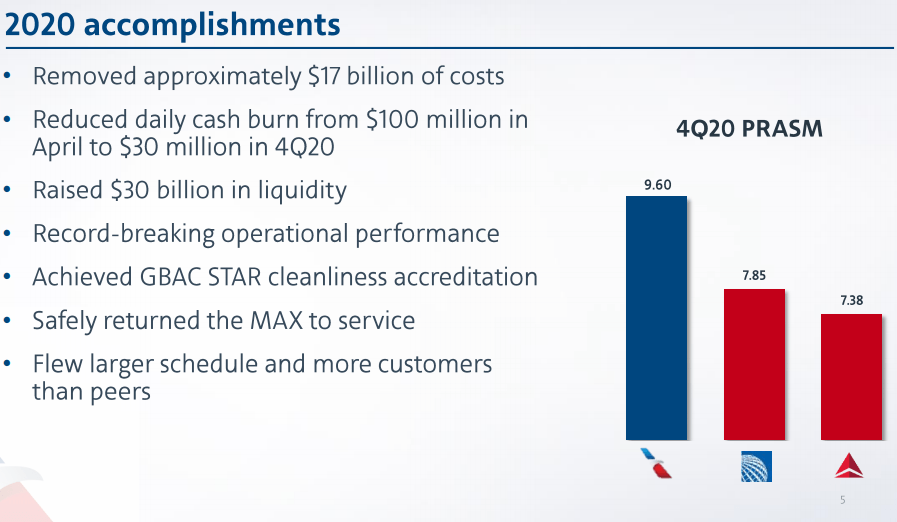

Last year was a horrendous, dark period in human history, and amidst our collective fervor in trying profit from moves in the market, it is easy to forget the suffering that befell the world in 2020.Part of that suffering was job losses that accrued from massive losses in places like airlines, which American certainly partook in. We're all aware of how poorly American performed last year so I don't need to rehash it, but on the bright side, some good came of it.

Source: Investor presentation

American removed $17 billion (!) in costs in 2020, and reduced its daily cash burn by 70% from the worst of the pandemic to the end of the year. This, of course, was a massive concern in the early stages of the crisis because airlines have enormous infrastructure that is costly to operate, which includes payroll. However, government measures and capital raises have kept the airlines afloat, and in my view, there are no liquidity/solvency concerns for American at this point. That's good, but it doesn't make the stock a buy; it just means there is no impending disaster.

Speaking of disaster, revenue could certainly be described as such for last year.

American had been producing nice, steady growth in the top line in the years prior to 2020, but of course, that all came tumbling down beginning in mid-March. Revenue was but a tiny fraction of what it was supposed to be, and even this year, which should see some return to normal, expected revenue is still just over half what it was in 2019. 2022 is slated to show another sizable rebound, but still nothing close to what American produced pre-pandemic.

Revisions aren't exactly bullish, either. In fact, revenue for this year continues to fall, even after the vaccine was announced. The timetable for a return to a normal flight schedule continues to be pushed back, and the revision trends above show you what that looks like in practice.

Buyers of the stock today - at very close to pre-pandemic levels - are essentially betting that these numbers suddenly reverse higher and take earnings with them; I'm simply unwilling to do that based upon the evidence I see.

Now, bookings are undoubtedly improving, and that's good news for a variety of reasons, whether you're a shareholder or not. We all want "normal" to come back and this data is a step in the right direction. But let's keep in mind that traffic is still less than half what it was in 2019, and that bookings for American continue to trend well below pre-pandemic levels. These numbers will continue to improve, undoubtedly, but we are still simply trying to get off the bottom. Bidding the stock up to new 52-week highs because a little bit of recovery is taking place seems extremely premature to me.

Here's an interesting look at where American sees the recovery, and again, I think it just points to how premature the rally in the shares is at this point.

I don't need to read this to you but basically, American is a very long way from a return to normal. And if we consider the domestic business stage of the recovery, it stands to reason that at least some of that traffic may never return. The world has proven it can operate without face-to-face interaction, so will companies continue to spend billions of dollars collectively on air travel that can be largely replaced with a video call? I don't think so, but American is pricing that in.

To be fair, American is almost certain to see margin improvements whenever "normal" comes back.

Not only does it have the cost savings identified above, but it has accelerated its fleet renewal/retirement program, so its fleet should be far more efficient in the coming years than it was going into the crisis. Those are good things, and should not be ignored. However, as we'll see below, based upon where the revenue situation is related to the valuation of the stock, these margin improvements simply aren't enough.

More Concerns

First up, American has nearly $30 billion of net debt following the emergency measures it undertook in 2020.American has always carried a huge amount of debt, but this problem has been exacerbated by the crisis. The company is paying more than a billion dollars annually just to service debt, and longer term, there is simply no capacity for this company to ever pay off a meaningful amount of it. Even if American simply wants to get back to its pre-crisis level of net debt, it needs to come up with ~$8 billion, or about 2.5 years of pre-crisis annual operating income. It will also make it more difficult for American to borrow in the future because it is already hugely leveraged at this point.

In addition, American has issued a sizable number of shares since the crisis began, as we can see below.

The share count has soared from 423 million a year ago to 640 million by December; I don't know what the share count will be for the end of March, but it won't be anything close to 423 million. That means massive dilution to shareholders, making an earnings recovery that much more difficult. Indeed, with 50% more shares outstanding, American has to now earn 50% more on a dollar basis to simply equal what the figure would have been under the old share count. Perhaps more than any other headwind, this one is significant.

For context, because of recent price movement and the higher share count, American's market cap is now higher than it was pre-crisis; that logically makes absolutely no sense given all of the problems American has today.

Let's Value This Thing

Obviously, American is going to produce another massive loss in 2021, but that is to be expected.Source: Seeking Alpha

Next year, consensus is for breakeven, roughly, followed by a small profit in 2023. By 2024, a normalized profit is expected, but that is three years from now. Bulls will surely look at the P/E ratio of 4.6 on 2024 earnings and lick their figurative chops, but as we can see below, that's not even that cheap.

This is a six-year look at American's forward P/E ratio prior to COVID-19, and should be a strong guide for how American will be valued coming out of the crisis. We can see that the lower bound was just over 4X, with the upper bound at 11X. Average was in the middle at 7X earnings, but let's keep in mind that American is trading for 4.6X projected earnings for three years from now. On that basis, the stock looks incredibly expensive to me, particularly considering the following: an uncertain future of business travel, nearly $30 billion in net debt, and an as yet undetermined return to normal time frame.

Putting all of this together, and a nearly full valuation on 2024 earnings estimates, the signal is clear; American is grossly overvalued, and the stock is a sell.

This article was written by

Josh Arnold

03-20-2021 | 05:33 AM

#419

Line Holder

Joined: Mar 2015

Posts: 77

Likes: 0

Did any of you actually listen to him at the JP Morgan Industrials Conference? Go all the way through to the Q&A.

If not here you go: https://americanairlines.gcs-web.com...als-conference

Make up your own minds all you airline profitability experts.

If not here you go: https://americanairlines.gcs-web.com...als-conference

Make up your own minds all you airline profitability experts.

03-20-2021 | 05:37 AM

#420

Line Holder

Joined: Jan 2014

Posts: 1,550

Likes: 146

Here's another expert on how eff'd we're all are:

(please click on the link, I can only post with three pictures, the article has about 10 graphs)

link

There was, perhaps, no industry more impacted by COVID than airlines. Of course, many types of businesses - particularly travel-related ones - were devastated by the faucet simply being turned off in a series of unprecedented moves by governments globally. Airlines, however, operate in a cut-throat, razor-thin margin business during good times, so 2020 was particularly nasty for them.

However, the light has appeared at the end of the tunnel, beginning with November's announcement that a successful vaccine was on the way. Since then, shares of coach class legend American Airlines Group (AAL) have more than doubled.

Indeed, if we draw a line in the sand in early November of last year, we can see that the airlines as a group have outperformed the S&P 500 by about 25%, and on top of that, American has outperformed the airlines by about 20%. In other words, American is flying (bad joke: I'll see myself out).

However, if we zoom out to the two-year chart above, we can see that there should be significant selling pressure on American in the near term simply because all of the people that bought in 2019 will now be at the point where they have more or less gotten their money back. Normally when a stock sees a massive decline and then recovery, price action churns when the stock returns to pre-crash levels. I expect that the enormous amount of supply in the mid-20s and up will be a problem for bulls. That doesn't mean American is doomed, but it does mean that the likelihood of this rally continuing at its current pace is extremely unlikely.

Apart from that, I just think American is very expensive, and is pricing in a recovery that may or may not come. In addition to that, the recovery is already years away under a rosy scenario; what if things don't work out as planned? For these reasons, I think American should be sold. I won't go as far as saying I'm bearish because airline stocks with high short interest are battlegrounds today, and anything can happen. But for long-term shareholders, your money deserves better; permit me to elaborate.

Part of that suffering was job losses that accrued from massive losses in places like airlines, which American certainly partook in. We're all aware of how poorly American performed last year so I don't need to rehash it, but on the bright side, some good came of it.

Source: Investor presentation

American removed $17 billion (!) in costs in 2020, and reduced its daily cash burn by 70% from the worst of the pandemic to the end of the year. This, of course, was a massive concern in the early stages of the crisis because airlines have enormous infrastructure that is costly to operate, which includes payroll. However, government measures and capital raises have kept the airlines afloat, and in my view, there are no liquidity/solvency concerns for American at this point. That's good, but it doesn't make the stock a buy; it just means there is no impending disaster.

Speaking of disaster, revenue could certainly be described as such for last year.

American had been producing nice, steady growth in the top line in the years prior to 2020, but of course, that all came tumbling down beginning in mid-March. Revenue was but a tiny fraction of what it was supposed to be, and even this year, which should see some return to normal, expected revenue is still just over half what it was in 2019. 2022 is slated to show another sizable rebound, but still nothing close to what American produced pre-pandemic.

Revisions aren't exactly bullish, either. In fact, revenue for this year continues to fall, even after the vaccine was announced. The timetable for a return to a normal flight schedule continues to be pushed back, and the revision trends above show you what that looks like in practice.

Buyers of the stock today - at very close to pre-pandemic levels - are essentially betting that these numbers suddenly reverse higher and take earnings with them; I'm simply unwilling to do that based upon the evidence I see.

Now, bookings are undoubtedly improving, and that's good news for a variety of reasons, whether you're a shareholder or not. We all want "normal" to come back and this data is a step in the right direction. But let's keep in mind that traffic is still less than half what it was in 2019, and that bookings for American continue to trend well below pre-pandemic levels. These numbers will continue to improve, undoubtedly, but we are still simply trying to get off the bottom. Bidding the stock up to new 52-week highs because a little bit of recovery is taking place seems extremely premature to me.

Here's an interesting look at where American sees the recovery, and again, I think it just points to how premature the rally in the shares is at this point.

I don't need to read this to you but basically, American is a very long way from a return to normal. And if we consider the domestic business stage of the recovery, it stands to reason that at least some of that traffic may never return. The world has proven it can operate without face-to-face interaction, so will companies continue to spend billions of dollars collectively on air travel that can be largely replaced with a video call? I don't think so, but American is pricing that in.

To be fair, American is almost certain to see margin improvements whenever "normal" comes back.

Not only does it have the cost savings identified above, but it has accelerated its fleet renewal/retirement program, so its fleet should be far more efficient in the coming years than it was going into the crisis. Those are good things, and should not be ignored. However, as we'll see below, based upon where the revenue situation is related to the valuation of the stock, these margin improvements simply aren't enough.

American has always carried a huge amount of debt, but this problem has been exacerbated by the crisis. The company is paying more than a billion dollars annually just to service debt, and longer term, there is simply no capacity for this company to ever pay off a meaningful amount of it. Even if American simply wants to get back to its pre-crisis level of net debt, it needs to come up with ~$8 billion, or about 2.5 years of pre-crisis annual operating income. It will also make it more difficult for American to borrow in the future because it is already hugely leveraged at this point.

In addition, American has issued a sizable number of shares since the crisis began, as we can see below.

The share count has soared from 423 million a year ago to 640 million by December; I don't know what the share count will be for the end of March, but it won't be anything close to 423 million. That means massive dilution to shareholders, making an earnings recovery that much more difficult. Indeed, with 50% more shares outstanding, American has to now earn 50% more on a dollar basis to simply equal what the figure would have been under the old share count. Perhaps more than any other headwind, this one is significant.

For context, because of recent price movement and the higher share count, American's market cap is now higher than it was pre-crisis; that logically makes absolutely no sense given all of the problems American has today.

Source: Seeking Alpha

Next year, consensus is for breakeven, roughly, followed by a small profit in 2023. By 2024, a normalized profit is expected, but that is three years from now. Bulls will surely look at the P/E ratio of 4.6 on 2024 earnings and lick their figurative chops, but as we can see below, that's not even that cheap.

This is a six-year look at American's forward P/E ratio prior to COVID-19, and should be a strong guide for how American will be valued coming out of the crisis. We can see that the lower bound was just over 4X, with the upper bound at 11X. Average was in the middle at 7X earnings, but let's keep in mind that American is trading for 4.6X projected earnings for three years from now. On that basis, the stock looks incredibly expensive to me, particularly considering the following: an uncertain future of business travel, nearly $30 billion in net debt, and an as yet undetermined return to normal time frame.

Putting all of this together, and a nearly full valuation on 2024 earnings estimates, the signal is clear; American is grossly overvalued, and the stock is a sell.

This article was written by

Josh Arnold

(please click on the link, I can only post with three pictures, the article has about 10 graphs)

link

American Airlines Has Problems On Top Of Problems

Mar. 19, 2021 11:39 AM ETAmerican Airlines Group Inc. (AAL)17 Comments2 LikesSummary

- AAL continues to rally hard.

- But, I see lots of resistance just above the current price.

- In addition, there are several fundamental reasons the current rally should not be supported.

There was, perhaps, no industry more impacted by COVID than airlines. Of course, many types of businesses - particularly travel-related ones - were devastated by the faucet simply being turned off in a series of unprecedented moves by governments globally. Airlines, however, operate in a cut-throat, razor-thin margin business during good times, so 2020 was particularly nasty for them.

However, the light has appeared at the end of the tunnel, beginning with November's announcement that a successful vaccine was on the way. Since then, shares of coach class legend American Airlines Group (AAL) have more than doubled.

Indeed, if we draw a line in the sand in early November of last year, we can see that the airlines as a group have outperformed the S&P 500 by about 25%, and on top of that, American has outperformed the airlines by about 20%. In other words, American is flying (bad joke: I'll see myself out).

However, if we zoom out to the two-year chart above, we can see that there should be significant selling pressure on American in the near term simply because all of the people that bought in 2019 will now be at the point where they have more or less gotten their money back. Normally when a stock sees a massive decline and then recovery, price action churns when the stock returns to pre-crash levels. I expect that the enormous amount of supply in the mid-20s and up will be a problem for bulls. That doesn't mean American is doomed, but it does mean that the likelihood of this rally continuing at its current pace is extremely unlikely.

Apart from that, I just think American is very expensive, and is pricing in a recovery that may or may not come. In addition to that, the recovery is already years away under a rosy scenario; what if things don't work out as planned? For these reasons, I think American should be sold. I won't go as far as saying I'm bearish because airline stocks with high short interest are battlegrounds today, and anything can happen. But for long-term shareholders, your money deserves better; permit me to elaborate.

American Is Doing What It Can

Last year was a horrendous, dark period in human history, and amidst our collective fervor in trying profit from moves in the market, it is easy to forget the suffering that befell the world in 2020.Part of that suffering was job losses that accrued from massive losses in places like airlines, which American certainly partook in. We're all aware of how poorly American performed last year so I don't need to rehash it, but on the bright side, some good came of it.

Source: Investor presentation

American removed $17 billion (!) in costs in 2020, and reduced its daily cash burn by 70% from the worst of the pandemic to the end of the year. This, of course, was a massive concern in the early stages of the crisis because airlines have enormous infrastructure that is costly to operate, which includes payroll. However, government measures and capital raises have kept the airlines afloat, and in my view, there are no liquidity/solvency concerns for American at this point. That's good, but it doesn't make the stock a buy; it just means there is no impending disaster.

Speaking of disaster, revenue could certainly be described as such for last year.

American had been producing nice, steady growth in the top line in the years prior to 2020, but of course, that all came tumbling down beginning in mid-March. Revenue was but a tiny fraction of what it was supposed to be, and even this year, which should see some return to normal, expected revenue is still just over half what it was in 2019. 2022 is slated to show another sizable rebound, but still nothing close to what American produced pre-pandemic.

Revisions aren't exactly bullish, either. In fact, revenue for this year continues to fall, even after the vaccine was announced. The timetable for a return to a normal flight schedule continues to be pushed back, and the revision trends above show you what that looks like in practice.

Buyers of the stock today - at very close to pre-pandemic levels - are essentially betting that these numbers suddenly reverse higher and take earnings with them; I'm simply unwilling to do that based upon the evidence I see.

Now, bookings are undoubtedly improving, and that's good news for a variety of reasons, whether you're a shareholder or not. We all want "normal" to come back and this data is a step in the right direction. But let's keep in mind that traffic is still less than half what it was in 2019, and that bookings for American continue to trend well below pre-pandemic levels. These numbers will continue to improve, undoubtedly, but we are still simply trying to get off the bottom. Bidding the stock up to new 52-week highs because a little bit of recovery is taking place seems extremely premature to me.

Here's an interesting look at where American sees the recovery, and again, I think it just points to how premature the rally in the shares is at this point.

I don't need to read this to you but basically, American is a very long way from a return to normal. And if we consider the domestic business stage of the recovery, it stands to reason that at least some of that traffic may never return. The world has proven it can operate without face-to-face interaction, so will companies continue to spend billions of dollars collectively on air travel that can be largely replaced with a video call? I don't think so, but American is pricing that in.

To be fair, American is almost certain to see margin improvements whenever "normal" comes back.

Not only does it have the cost savings identified above, but it has accelerated its fleet renewal/retirement program, so its fleet should be far more efficient in the coming years than it was going into the crisis. Those are good things, and should not be ignored. However, as we'll see below, based upon where the revenue situation is related to the valuation of the stock, these margin improvements simply aren't enough.

More Concerns

First up, American has nearly $30 billion of net debt following the emergency measures it undertook in 2020.American has always carried a huge amount of debt, but this problem has been exacerbated by the crisis. The company is paying more than a billion dollars annually just to service debt, and longer term, there is simply no capacity for this company to ever pay off a meaningful amount of it. Even if American simply wants to get back to its pre-crisis level of net debt, it needs to come up with ~$8 billion, or about 2.5 years of pre-crisis annual operating income. It will also make it more difficult for American to borrow in the future because it is already hugely leveraged at this point.

In addition, American has issued a sizable number of shares since the crisis began, as we can see below.

The share count has soared from 423 million a year ago to 640 million by December; I don't know what the share count will be for the end of March, but it won't be anything close to 423 million. That means massive dilution to shareholders, making an earnings recovery that much more difficult. Indeed, with 50% more shares outstanding, American has to now earn 50% more on a dollar basis to simply equal what the figure would have been under the old share count. Perhaps more than any other headwind, this one is significant.

For context, because of recent price movement and the higher share count, American's market cap is now higher than it was pre-crisis; that logically makes absolutely no sense given all of the problems American has today.

Let's Value This Thing

Obviously, American is going to produce another massive loss in 2021, but that is to be expected.Source: Seeking Alpha

Next year, consensus is for breakeven, roughly, followed by a small profit in 2023. By 2024, a normalized profit is expected, but that is three years from now. Bulls will surely look at the P/E ratio of 4.6 on 2024 earnings and lick their figurative chops, but as we can see below, that's not even that cheap.

This is a six-year look at American's forward P/E ratio prior to COVID-19, and should be a strong guide for how American will be valued coming out of the crisis. We can see that the lower bound was just over 4X, with the upper bound at 11X. Average was in the middle at 7X earnings, but let's keep in mind that American is trading for 4.6X projected earnings for three years from now. On that basis, the stock looks incredibly expensive to me, particularly considering the following: an uncertain future of business travel, nearly $30 billion in net debt, and an as yet undetermined return to normal time frame.

Putting all of this together, and a nearly full valuation on 2024 earnings estimates, the signal is clear; American is grossly overvalued, and the stock is a sell.

This article was written by

Josh Arnold

Thread

Thread Starter

Forum

Replies

Last Post